|

GILLES BOUCHARD

"HP Global Operations"

HP industry analyst meeting

New York City

December 14, 2005

© Copyright 2005 Hewlett-Packard Development Company, L.P

All rights reserved. Do not use without written permission from HP.

Good morning, everybody. My name is Gilles Bouchard, and I manage Operations for HP. You heard a lot today about the great portfolio of products we have. You heard a lot about our great customer base, and Cathy Lyons showed you how we go to market through four major routes, along the value and the volume dimension and the direct and indirect dimension.

What I want to do now is show you how this works operationally. As you can imagine, this presents unique challenges and unique opportunities from an operational point of view. I’ll take you behind the scenes and show you how it works.

I’m going to talk about three things today. The first thing I’ll talk about is execution. How we execute in Global Operations. Next, I’m going to talk about cost. How we are driving out cost. Finally, I’m going to give three examples that show you how we use the portfolio of different supply chains to bring unique value to customers and to the market.

Let me start with Cathy’s first slide. This is the portfolio of the customers and the four routes to market. I’ll show you how we have architected this from a supply chain point of view to fulfill this go-to-market model.

If you break it down into the four basic elements of a supply chain, from left to right you have procurement; manufacturing; demand fulfillment, which is logistics and distribution; and demand management. Demand management is all the customer facing operations, such as e-commerce, catalogs, order management, pricing, etc.

We have organized our supply chain around six major modules – three customer-facing modules and three product modules. The three product modules are aligned with the three business groups – PSG, IPG, and TSG – with some shared procurement across the company. We procure about 40% of our parts shared across the company. The customer-facing aspects are aligned along value, volume direct, and volume indirect.

Let me make two points. First, this is not a one-size-fits-all supply chain. That wouldn’t work for this company. It wouldn’t serve our purposes. On the other hand, it’s not a free for all. It is not 20, 30, 40 different supply chains. It’s a modular supply chain with six very specific modules – three customer-facing, three product-centric.

The second aspect, where we’ve changed a lot, is from a ‘product-out’ to a ‘customer-in’ approach to the supply chain. It’s no longer about building products and pushing them to the market through as many channels as possible. It’s about studying the customer; building a solution for that customer; then bringing all the elements of HP’s portfolio necessary to build a solution for this customer through a set of supply chains and routes to market.

So let’s start with execution. Execution is job #1. It’s an area where we’ve done a lot of work last year and we’re happy to report good progress. We’ve changed our accountability model. We’ve created empowered executives in each region that can bring all the elements of our supply chain together and fix the issues.

We’ve done a lot of work on business control around pricing. We’ve developed tools to track deal profitability day-by-day. We’ve seen improvements in margin due to the back-office operations work we’ve done.

One of the most important metrics is cycle time for direct orders which depends on executing well across the whole value chain. If anything goes wrong in your value chain, whether it’s procurement, manufacturing, or customer-facing order fulfillment it shows up right away in direct order cycle time. We have a six-point program that improved the cycle times by 50%.

It’s always easy to improve delivery of products when you increase inventory. It’s important to keep a balance. We decreased inventory as we improved delivery performance.

Now look at the how this translated into customer satisfaction. We put together a team that tracked and managed our global accounts, to track escalations and issues, etc. We’ve seen a decrease in issues by 60%. We’ve seen a decrease in time to resolve issues by 33%, and almost complete disappearance of what we call red hot issues, which are the highest level of escalations that we have. So good progress in this area.

We surveyed the broader base of customers. In the enterprise space, we’ve seen a 20% increase in customer satisfaction. Delivery performance, which was a sales inhibitor last year, is starting to show up as an element of loyalty to HP, which is very good news for us. We’re starting to see the same thing on the channel side where surveys’ shows a 15% improvement.

So good progress. We’re not done yet. This is something that will never stop. I believe in a relentless focus on execution. We’re continuing our six point program on cycle times. We have all kinds of work we’re doing on supply chains, but again we’re glad with the direction and we’re going to continue that effort. So that’s execution. Now let me talk about cost.

Last year our goal was to take a billion dollar of cost every year out of the end-to-end operational engine. I’m pleased to tell you we accomplished that. The big news is that we are going to do this for the next two years as well.

Let me break down how we do this. There are three major components that we go after. One is the cost of products, the cost of goods sold, the procurement and supply chain cost. Next there’s indirect procurement. Finally, the cost of the front-end piece of the supply chain. Let’s start with the cost of products.

As you can see, we took about $500 million out of procurement. These procurement numbers can be very misleading. Companies could go out and claim billions of dollars savings in procurement, but we always try to take out the market component of the procurement reductions. As you can see, last year the market went down quite a bit as commodity prices fell rapidly. So we enjoyed more than $2 billion in cost reduction – all technology vendors get this. What really matters are savings we get that other people don’t get, which was about $500 million.

Looking forward, we’re projecting similar advantage procurement of between $3- and $500 million, based on two simple things: one, we leverage our size. Secondly, we have a highly consolidated supply chain. To give you an idea, about 90% of our spend is with our top 50 suppliers. So it allows us to have very specific procurement agreements.

We did extensive benchmarking of our procurement last year. We found that we didn’t have to invent anything new. We have four or five world-class best practices in procurement, but they were not used enough across the company. We don’t need to change what we do, but do more of it.

If you remember the four columns I had in the graphic, procurement is the cost of the left column. Supply chain is the two middle columns – manufacturing and distribution. We actually saved less money in supply chain operations last year than the year before, but looking forward, we are going to run that back up again to $3- to $500 million range.

Last year saw the end of the massive merger-related supply chain initiatives. We’re now in a second wave of investment across the company, across all the businesses. There are very aggressive plans to cut supply chain costs and manufacturing costs. I’ll give you a couple of examples. First, IPG has a very aggressive program to move from a two-step supply chain to a one-step supply chain. Second, we plan to cut our number of warehouses by 30-40% next year.

Finally, if you look at the cost savings in supply chain and procurement, they don’t necessarily correlate directly to the improvement in gross margins. The reason why gross margin went up so much last year (a 3x improvement) is in part because of the supply chain and procurement savings, but even more because of how we managed pricing, mix management, etc. All those elements are critical to our success.

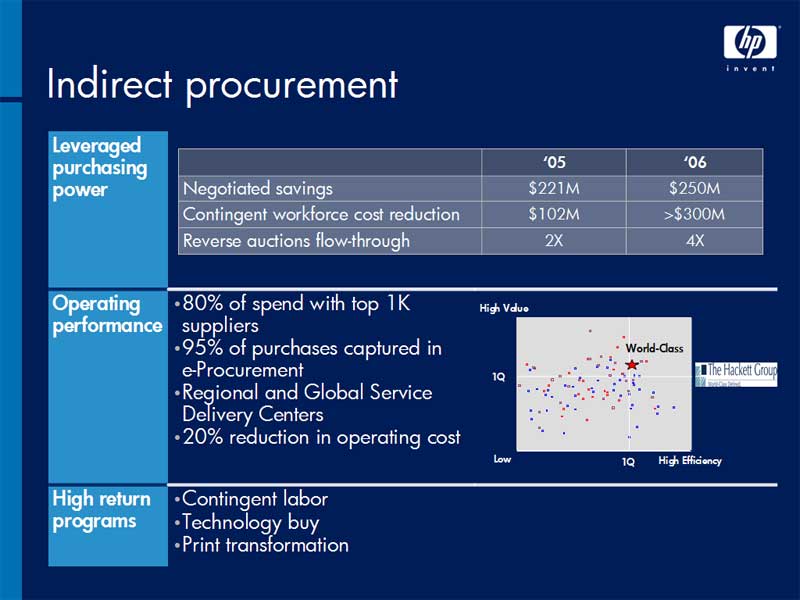

The second element of cost I want to talk about is indirect procurement. The negotiated savings were in the range of $220 million. We also launched a program in June, started by Mark Hurd, to significantly reduce the use of consultants in the company, which saved a hundred million dollars.

I look at indirect procurement as a three-step process. The first step is transactional. We make sure we capture as much of the spend as possible, so we can apply business controls. We captured 95% of the spend across the company. Next, we use procurement techniques to reduce and aggregate suppliers, and by renegotiating contracts. So that’s where this $220 million savings comes from. Next year this will be an even bigger number. The third step is to start engaging direct procurement directly with functional owners in the businesses on specific strategic initiatives. The consultant reduction was one. We’re very engaged with Randy Mott and his team in reducing the technology spend across IT. We have an initiative to roll out some of the print services that VJ talked about across the company. The strategic engagement on the procurement side yields additional returns.

We benchmark well on operating performance and our direct procurement capabilities. We have a plan to reduce our own internal cost by 20% this year to bring it to world-class, while delivering the same capabilities.

The third element of cost is the route to market. This is the column that was on the furthest right of the opening chart. It’s the customer-facing operations. We measure savings in route to market between volume direct, volume indirect, and value. We’re looking at saving at least $50 million over the next two years in this area.

This number might look small compared to the other numbers, but it’s very important for two reasons. One, this is controllable direct expenses. So we can redirect these savings to better sales coverage or to the bottom line right away. Second, because of the change of mix and because of the growth of the company, if we kept that ’05 cost structure through ’07 with the ’07 mix in volume, it would not go down by $50M; it would go up by $200M. So it is critical for us to stay ahead of the cost curve because of the mix and the volume changes.

There are three main initiatives. First, a major change in workforce deployment. To keep in-country only the high-touch customer interaction resources. The back office is already pretty much all offshore, and we’re developing large near-shore centers that provide proximity and language skills for those activities.

Second, we globalize and simplify processes. You hear this across the company. We’re working very intensely on it. This drives a lot of IT simplification and reductions as well.

Third, we’re looking at leverage across the routes to market, which used to be managed fairly independently. Now we’re starting to combine some capabilities across them.

On the indirect side, the decrease is smaller. It’s only 8%. But it’s large on an overall scale. The back office is already all off-shored. It’s highly automated. The reduction really comes from the near-shore support of some of the activities.

On the volume direct side there’s been a big decrease. This is very strategic for us. It’s a fast growing route to market. We’ve invested a lot in automation, in new tools. We will continue this over the next two years. There’s a lot fixed cost and very low variable costs. So we can observe a lot of growth without increasing the cost too much.

On the value side, this is a much more country based, labor intensive process. So it’s benefiting from all of the three initiatives – optimization of the workforce deployment, globalization of processes, as well as we’re finding good leverages between volume and value direct.

That’s it on cost. Enough of the numbers. I want to close by sharing three examples on how this portfolio supply chain helps us create more value. I’m going to start with a simple example where we use one supply chain and build it into an example where we use all of them together.

The first one I want to use is the Wal-Mart Black Friday example. I suspect many of you know about Black Friday. Maybe some of you were in the stores at 5AM. I’m not going to ask if any of you were involved in the brawls or melees that happened that morning, but it got a lot of press this year. It’s the launch of the holiday season, and retailers – Wal-Mart in particular – create incredible value for customers by working with HP, which draws huge crowds to their stores.

This is an incredible logistical and supply chain challenge. We’ve won this for eight years in a row because of our ability to execute. As you can imagine, hundreds of thousands of products need to be delivered within very narrow windows, with very long planning cycles. The planning cycles start almost a year ahead of time with procurement, bringing strategic partners onboard, and so forth, all culminating in the last few days where everything has to hit the 3,000 stores at the same time.

If you talk to the customer, Wal-Mart, and ask them why HP? They’ll say, first, the ability to put great value on a top branded product. Second, third, and fourth is execution, execution, execution. We’ve always come through for them on this with massive volumes, hundreds of trucks. It’s to the point that, when we start shipping these products, we have to work with law enforcement so that they can regulate traffic for us because we put so many trucks on the road. That’s the level of detail we have to manage.

This is an example of one supply chain of our portfolio being very competitive. Again, the idea of having a portfolio supply chain only works if each one of them stands on its own, and then the sum of them brings an advantage.

Now let me move to a different example where we implement two supply chains. Akzo Nobel is a very large pharmaceutical company out of the Netherlands. They required global deployment of a set of volume products – notebooks, desktops, servers, printers – to 78 countries and 850 sites. This started as your standard large-scale PC deal, multiple vendors, huge negotiation, very focused on cost. We’re able to bring a couple of unique capabilities to the customer.

Through our volume direct operation, we were able to ship directly to about half of the countries, but for the other countries where nobody can ship direct, we were able to bring in channel partners that can give us this reach. We did this with consistency, with one customer interface, one HP.com product portal, one global catalog. And most importantly for the customer, one set of reports. They know daily everything that we’ve shipped, whether it’s directly from HP or through a partner.

So it’s not just about using the partner. It’s the seamless integration of information between HP and our partners that brought a unique advantage to us. It started as a really tough negotiation. We have now more than 80% share in this account because the value that we bring by enabling a global account, a global catalog, and the fact that the procurement team can now micromanage everything that’s happening and enforce plans across the company. This brought them much more value than anything else. So that’s two supply chains.

The final example is a pretty exciting story which happened about a year ago with DHL – a big customer of ours which brought just about everything we had to the table. DHL is a large company with a country-based legacy affected by mergers. Challenges similar to those HP face and that Randy Mott will talk about. They built a green-field data center in the Czech Republic. This datacenter combined systems which were in hundreds of different places before.

They needed value products. About 500 unique servers, major disk arrays. They needed volume products – desktop, notebooks, Intel servers. They also needed printers. We did a print on demand operation for them. So everything. They used the whole HP product portfolio, all brought together through HP Services.

We used the same volume direct approach as for Akzo Nobel to bring all the volume products to them – the same reporting and the same type of portal – but on top of it, because this was a large service-led value deal, we drew upon two other supply chains. The printing products went through a pure channel model, and all the value products went through the value direct model. And all of this was managed within one account team, one set of reports, one set of programs.

So we used three customer facing supply chains and three product supply chains, all integrated in one project. All done within two months. It was a huge project, a huge risk for DHL. And by concentrating all our supply chains and capabilities we brought their CIO Steven McGuckin all the elements that he needed within 60 days to successfully launch his data centers.

I will close by reminding you of the three things that are important for us – relentless daily focus on operations, taking a billion dollars of cost every year out of this whole space, and turning our portfolio of supply chains into a unique competitive advantage to create value for our customers.

Thank you.

|