|

GILLES BOUCHARD

"HP Global Operations and IT"

HP security analyst meeting

Boston, Massachusetts

December 7, 2004

© Copyright 2004 Hewlett-Packard Development Company, L.P

All rights reserved. Do not use without written permission from HP.

Thank you Mike [Winkler]. Good morning everybody, my name is Gilles Bouchard. This is my first time here, let me welcome all of you. I'm happy to be here.

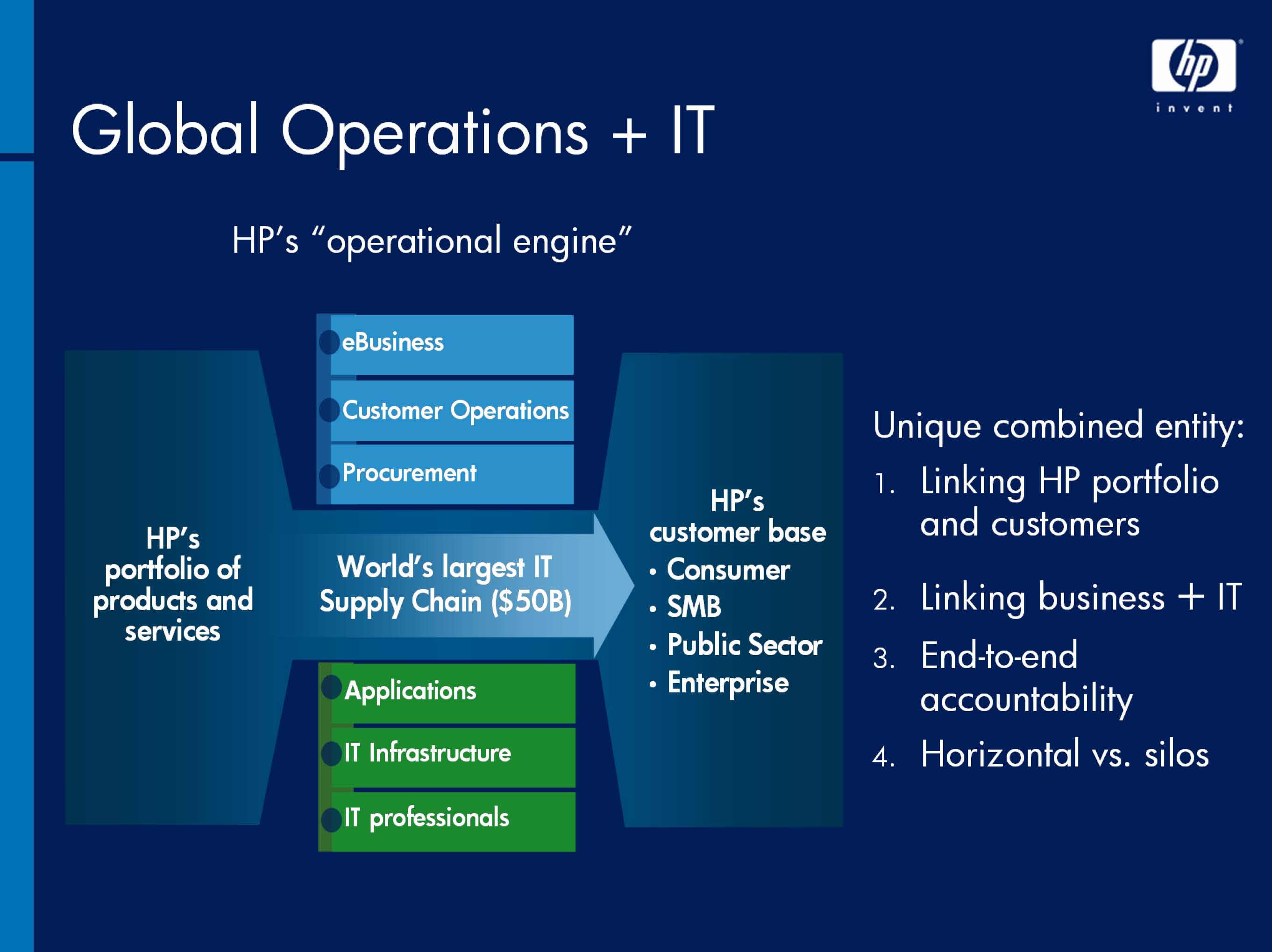

Global Operations and IT - we call it Global Ops and IT internally - this is a very new organization. It's also a fairly new concept in the industry. So I'm going to spend a few minutes first introducing the team and what we do.

Four main take-aways: First, the way I like to describe this team is it's the operational engine behind all the business and go-to-market capabilities of the company. We are the engine that links the great product portfolio we have to the great number of customers we serve. So number one, the link between the portfolio and our customers.

Number two, which is fairly new, our team is a combination of IT and business capabilities. We have activities such as a supply chain - a $50 billion supply chain - procurement, customer-facing operations in support of what Mike Winkler just talked about, eBusiness capabilities, as well as a whole portfolio of applications that is behind all of this, as well as the IT infrastructure, which we manage.

So we are very much aligned with the principles of the Adaptive Enterprise - a combined entity that links business and IT together.

Number three: End-to-end accountability. This was something that was very important to me when we brought the team together in December at a worldwide level. We made it a priority to also create and replicate this model at the operational level, as well as at the regional levels. So now we have a regional operations manager in each one of our geographies. And we have end-to-end accountability across the whole cycle from order to delivery for operational excellence. We put that in place in May and it's already showing a lot of great results for us.

Number four, it's a horizontal model in the sense that it's not a pure centralized and not a pure decentralized model. We are centralizing all the activities that are shared across the company, which is about 70 percent of what we do, but also we have a lot of activities that are decentralized across the company when they are specific to a given business.

And then we manage those across the company through common processes and tools. So that's Global Ops and IT.

Going back to number one, the link between the portfolio and our customers, let me give you a little bit more strategic color on this.

This is the engine that we are building for this company. On the one hand, we have a great portfolio; it is a unique portfolio in the industry. On the other hand, about a billion customers. Our role is to bring those together in a way that's consistent with the company's strategy. As you heard, our core strategy is based on the portfolio and is based on a customer-centric approach.

Historically, operational teams within HP were built more on a "product-out" point of view. We had GBU product-based capabilities which tended to be hard-wired across these value chains from products directly to customers, with no flexibility. So what we've done is basically turned this model around completely, and we've moved to a customer-first approach. The focus now is on building customer-centric capabilities, and I'll show you some examples of that. And that enables us to flow to customers the appropriate elements of the portfolio, based on what they need. I'll talk more about this customer dimension and the sales and marketing support side in a minute.

On the supply chain side, I think most of you have already been exposed to the concept of the five supply chains. We are building all our capabilities around five supply chain sets. Not 50 or 60 supply chains, like we used to have, which were product-based. But not one supply chain either. One would not be sufficient to enable the breadth of our portfolio and the breadth of our strategy. This is not a one-size-fits-all approach. It's a five-supply-chain model and again I think many of you have seen this before: This goes from "no touch," where products are delivered directly from supplier to customers, all the way up to "High Value and Solutions" involving complex configurations and "After Sales Services".

So this is the architecture we've used to build everything that we do in this organization. The way we measure progress is along a set of business metrics which fall into two major buckets: What I call efficiency - cost reductions - and what I call effectiveness, which is our ability to develop capabilities to grow the business and grow value. So let me first talk about the cost side, the efficiency side.

Some of you may be familiar with these historical cost-saving numbers. As you recall, we committed to $1.5 billion of savings across our operations from the merger. This number was achieved after one year. We then set another goal for the second year to do another billion dollars, which came out to about $1.4 billion. So great results.

It turns out that we believe we can carry a lot of those methodologies forward and create what I call this annual billion-dollar cost-reduction machine, with the goals that I show here.

A few comments: One of the questions that often comes up is, "Where does this money go?" So we've done some extensive modeling over the last year on our margin. And if you look at the last year of those savings, about 60 percent goes to pricing. In other words, enabling us to lower the price on a given product. Twenty percent goes to creating richer products - in other words, maintaining pricing power by putting more features and more capabilities into a given product, while maintaining the price. And then 20 percent went to the bottom line.

Second point, on this first line you can see direct material leverage. In this line, we exclude every market-driven cost reduction. So as you can see in the footnote, we exclude about 90 percent of our material cost reductions. We could stand up and claim $5 billion of cost reduction every year. But those numbers would be irrelevant because they would be purely market-driven reductions. So what we put in there is exclusively the reduction that represents the real savings we've achieved, above and beyond purely market-driven factors.

I want give you more color on the material and procurement side. On the supply chain side, to give you some idea of those numbers, there is a lot of simplification and rationalization work behind all of this. The number of manufacturing sites and distribution sites for example, those were reduced by a factor of two, sometimes a factor of three. And we believe there's still more potential there in the future.

Here's another way to look at those numbers: Last year our overall supply chain cost in dollars stayed flat, while we grew the business by $7 billion and shipped about 7 million more units. And as you know, this was in an environment where transportation costs were under huge pressure and the market prices went up. For example, ocean freight costs increased I think by more than 20 percent.

So now let's look at the procurement side. Three major areas: From a direct procurement point of view, obviously size is really important. We have the largest spend in the industry, about $43 billion. We have done a lot of work in aggregating that spend. About 90 percent of our spend is with our top 40 suppliers. So great progress there.

But beyond pure size, what we found out - and we've done several independent studies on this - is that we have developed over the years several core competencies and core processes which will help us carry this advantage forward.

I've got a few examples here. One that we call Buy/Sell. Buy/Sell is a process whereby we can control our spend and maintain aggregation of our spend even when we work through third party and contract manufacturers. That's a capability that a lot of our competitors are trying to emulate right now.

ESourcing, auctions, RFQs, co-planning, a lot of web-enabled capabilities which we are growing very rapidly. Procurement risk management: Here we have specific algorithm that we've developed and which we have patents on that enable us to match supply and demand variations in some key commodities. We have more than $6 billion of parts protected through this process. On and on and on.

And we've gained some recognition in these areas. You have the "Purchasing Magazine" award, which we won this year. That made HP the first company to win the gold medal twice. The last time was in '92. So a great honor and some great recognition for the achievement of our procurement team over the last two to three years.

Indirect procurement, a very similar story. We have aggregated our spend, so that about 95 percent of our indirect procurement spend flows through a centralized transactional engine. That allows us now to centrally negotiate more and more of the spend. You can see the numbers: About 55 percent of the spend centrally negotiatiated last year, going to 85 percent.

A lot of rationalization of the supply base. We've basically removed two-thirds of our suppliers over the last two years. And again, a lot more potential looking forward.

What's interesting about indirect procurement is we are now able to leverage this engine for more strategic programs. For example, last year we had a great and very successful program with Mike Winkler on marketing spend where we reduced our marketing supply base by more than 90 percent. That brought in some great cost reductions.

We have a joint program with VJ [Vyomesh Joshi] now on print management and a company-wide initiative on contingent labor.

Now, leveraging size and scale obviously matters from a procurement cost point of view. But it also matters a lot from an engineering and cost of engineering point of view. Every dollar of cost engineering can be leveraged over a broader base. And IPG [the Imaging and Printing Group] is a great example of that, where they generated more than $200 million of cost savings through cost of engineering, parts re-qualification, parts redesign.

Because of their lager base, they have a much bigger ROI on these programs. Let me give you an example, I looked at a couple of these programs. They saved five cents per printer with a project on ABS plastic resin. But that was over 20 million printers. So that's where scale matters.

They saved 35 cents per printer on LCD panel products. But that was leveraged over 10 million printers. So you can see, size and scale really matter from an innovation point of view, not just from a procurement leverage point of view.

Along the same vein of innovation, we have also created a very proactive and thorough program in the area of product and part simplification. What we call design for supply chain. We have 45 official programs across the company. I included just three examples here.

In business PCs for example, almost a 50 percent reduction in SKUs this year, leading not only to cost reductions but better service levels and cycle times. We have an ongoing project in the enterprise server space and a lot of projects as well in IPG, including the one I mentioned in part simplification. A huge savings potential here looking forward. So again, innovation and procurement leverage from a scale point of view.

So that covers the cost reduction piece, now let me move to the IT piece. From an IT point of view, what this chart summarizes is a very simple strategy, which is to reduce the total cost of IT as a percentage of revenue, while at the same time increasing the amount of IT money we spend on innovation and business capabilities. So this is the effectiveness part of our strategy.

Here's where we are today: Already a lot of good progress. We have reduced IT spend from 4.6 percent to 3.6 percent of revenue while increasing the innovation piece from 25 percent to 35 percent.

We've done this through major IT aggregation and consolidation. To give you some idea, we went from 7,000 applications to about 4,000. And 300 data centers to 85 data centers. Twenty-five thousand servers to 19,000 servers. And the list goes on.

Now what we realize is that there's only so much you can do by transforming IT purely from an IT point of view. To go to the next level, the transformation has to come from a business process point of view. And by the same token, when we go to customers and talk about the Adaptive Enterprise, we are applying this same rule internally - it's about transforming the company from a business process standpoint.

So as we go to the next level, we're going to take IT costs to less than 3 percent, innovation to more than 50 percent. To do that, we are now taking a business process approach to the transformation.

And what we've done is we have looked at all the processes across the company, we've looked at 114 different processes in all, and we looked at how much commonality we wanted across those processes, from a top-down point of view, and here's what we've found.

We've found that a reasonable target is to have almost 70 percent commonality in our processes across the company. Not one size fits all, it's different by functional area. HR for example is almost 100 percent, while supply chain is lower because it has a stronger product component. But this is the target architecture we're driving the company towards. This is what we call the business process architecture.

And let me show you our progress in terms of where we are today. In some areas we're done, like HR. Some areas we still have a lot of potential ahead of us. So this is the final transformation that we're driving throughout the company from the process and business processes point of view.

Let me show you a couple of examples. HR: I don't have the chart, but it's an interesting example because we are basically done. This was a top-down driven mandate to move everything to global processes. Thirty six different processes, globally delivered through the HR portal with just one single application. We run the biggest PeopleSoft application in the world now; it's a single database, single data center, all running on a virtualized infrastructure, eight Itanium servers. So you can see the whole transformation all the way from the strategy level and the business processes down to the server infrastructure.

This is the essence of the Adaptive Enterprise. This is what we're trying to leverage across the whole company.

Mike talked about some of the marketing capabilities. I just want to highlight a couple things in support of what he said. On the upper right here, we have rolled out a marketing resource management platform which will help marketing manage its spend the same way that we've been managing the spending in procurement and indirect procurement. So we are now capturing about 20 percent of our marketing spend, but this will grow rapidly over the next couple of years and will give us a lot more leverage on our marketing investment.

This spending is being used for much more personalized campaigns, which will drive higher cross-sell, a higher up-sell, something we've been doing for a while in consumer with great results as you can see. A good increase in attach rates here. We are now leveraging those capabilities into the SMB segment. Again, good initial results on this.

On the enterprise side, what we're doing is personalizing not only per customer but per user within the customer, with some very special algorithms that we've developed. Again, we have some target accounts that we are targeting this year. We saw a 30 percent increase in revenue already. This will be increased by five times next year to more accounts.

Then to close the loop, we put together a set of very strong analytics. We have several patents on those algorithms which help us close the loop on this whole marketing value chain and create this virtuous cycle where we understand our spend better, so we have more visibility, we target more relevance in terms of the user, which creates more margins and more cross sell. And then we have the insight to close the loop. So this is in support of what Mike talked about. It's a very, very exciting area and it is growing very rapidly for us.

On the sales side: Mike talked about this so I won't get into the details, but just a couple of points here. This is the biggest area of investment in terms of driving growth right now, in support of the sales transformation, sales productivity, growing our direct volume.

Very good alignment with Mike again from a business process and IT perspective. This is an area that we're using as a pilot and target for our business process architecture. So that we can quickly go to the target architecture and accelerate the transformation.

In conclusion, we are very much in sync with the principles of the Adaptive Enterprise, we are now driving the transformation of the company from a process-down point of view and linking business and IT together. This is what my team is all about, and it's starting to yield very exciting results for us.

We are taking all the learnings and expertise we've gained over the last two years from a cost-savings point of view, and we're leveraging those forward into this billion-dollar-a-year cost reduction machine. A key part of that is synchronizing and combining IT and operations. And last but not least, through our regional model, we're driving end-to-end accountability and a relentless focus on day-to-day execution.

That's it for me. Thank you.

|